Life insurance is a crucial element of financial planning, offering peace of mind and security for your future. Various options are available in life insurance that cater to different needs and preferences. Among these, term life insurance and money-back plans are popular choices, each with unique benefits. This article aims to shed light on why term life insurance could be a more beneficial option compared to money-back plans.

Term Life Insurance: Simplicity and Cost-Effectiveness

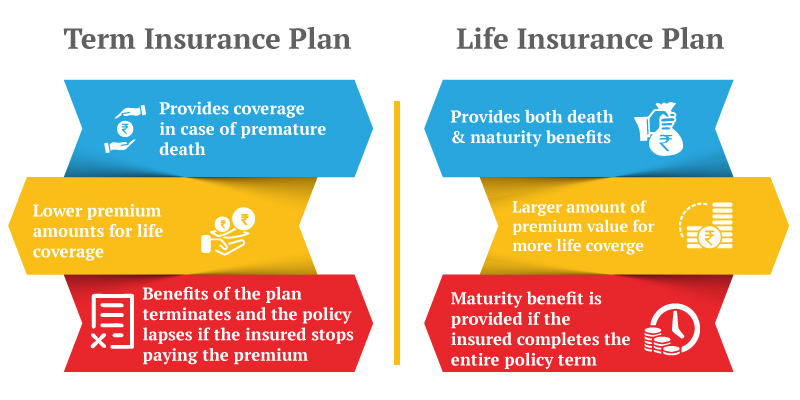

What is Term Life Insurance?

Term life insurance is a policy that provides coverage for a specified term or period. If the insured person passes away during this term, the beneficiaries receive the death benefit. One of the primary appeals of term insurance is its simplicity and focus on providing a substantial death benefit at relatively lower premiums.

Cost-Effectiveness

When it comes to affordability, term life insurance often stands out. Compared to money-back plans, the premiums for term life insurance are generally lower, offering a more budget-friendly approach to securing life coverage. This aspect is particularly appealing for young professionals and families starting out, who may be looking for robust coverage without straining their finances.

Additionally, options like a term plan with return of premium provide the dual benefit of affordability and the assurance of getting back the premiums if the policyholder survives the term, adding another layer of financial benefit. The lower cost of term insurance allows policyholders to allocate savings to other important financial goals, such as retirement planning or children’s education. This makes term life insurance not only accessible but a strategically sound choice for individuals seeking substantial coverage without a hefty price tag.

Additionally, options like a term plan with return of premium provide the dual benefit of affordability and the assurance of getting back the premiums if the policyholder survives the term, adding another layer of financial benefit. The lower cost of term insurance allows policyholders to allocate savings to other important financial goals, such as retirement planning or children’s education. This makes term life insurance not only accessible but a strategically sound choice for individuals seeking substantial coverage without a hefty price tag.

Money-Back Plans: Understanding the Differences

The Mechanism of Money Back Plans

Money-back plans are a type of life insurance policy where a portion of the sum assured is returned to the insured at regular intervals. This feature can be appealing to those looking for periodic returns alongside life coverage. However, this comes at a cost. These plans are structured to offer not just life protection but also a saving component, making them more complex than other insurance products. Furthermore, the return intervals can be a useful feature for managing short-term financial goals or obligations, providing a combination of security and savings.

Higher Premiums and Returns

The premiums for money-back plans tend to be higher than those for term life insurance. This is due to the added component of regular payouts. Additionally, the overall returns from money-back plans might not always be as competitive as other investment options. It’s important to consider that while these plans can offer regular financial returns, they cannot be your primary investment strategy. Higher premiums reflect the dual nature of these plans—insurance with investment—which might not be suitable for everyone.

Term Life Insurance: Flexibility and Payout

Policy Term Options

Term life insurance policies offer flexibility in choosing the policy term. This allows individuals to select a term that aligns with their life stage and financial goals. Whether it’s a 10-year, 20-year, or 30-year term, one can modify the policy duration to their needs. This adaptability is beneficial for life’s changing circumstances, such as starting a family or planning for retirement, ensuring that your coverage evolves with your life.

Larger Death Benefit

The focus of term life insurance is on providing a death benefit. That is, in the event of the policyholder’s untimely demise, beneficiaries receive a significant sum. This can be particularly important for those looking to ensure financial stability for their loved ones. Furthermore, the substantial payout can serve multiple purposes, from settling debts and mortgages to funding education and other long-term financial goals, offering a safety net for those you care about most.

Tax Benefits: An Added Advantage

Tax Savings under Term Life Insurance

Both term life insurance and money-back plans offer tax benefits under Section 80C of the Income Tax Act, allowing for deductions on premiums paid, up to a limit of ₹1.5 lakhs annually. This can result in significant tax savings, especially for those in higher income brackets.

The lower premiums of term life insurance enable policyholders to maximise their tax benefits efficiently. For instance, if a policyholder pays ₹20,000 annually for a term insurance premium, this amount is fully deductible from their taxable income, effectively reducing their tax liability. Furthermore, under Section 10(10D), the death benefit received from a term life insurance policy is generally tax-free, providing beneficiaries with the full amount without any deductions. This contrasts with certain other investment options, where returns might be subject to taxes.

Conclusion

Choosing between term life insurance and money-back plans depends on individual financial goals and needs. While money-back plans offer the dual benefit of insurance and periodic returns, term life insurance stands out for its simplicity, cost-effectiveness, and significant death benefit. It’s essential to assess your financial objectives and choose a plan that aligns with your long-term goals, ensuring peace of mind and financial security.

Read more :

- A Comprehensive Guide To Master Dental Billing

- Popular Fantasy Series To Binge-Watch This Weekend

- Why Cold Calling Still Matters In The Digital Age Of Real Estate Marketing?

- Branding Design: The Art Of Building Memorable Identities

- Success With Local SEO Services In NYC: Best Guide 2023

- The Best Android Apps For Retraining Your Brain In 2023